Activism Does Not Spare New CEOs

Activism is one of the forces behind the decline in CEO tenures, and it is reaching new CEOs earlier than most expect.

Rodolfo Araujo, CFA | April 24, 2025

The CEO role has been changing in two ways worth a new chief executive's attention. Tenures have been getting shorter, and the level of shareholder activism has been rising. Both were on clear display in 2025. Boards named 168 new S&P 1500 CEOs, the most since 2010, and the average tenure of a departing CEO eased to 8.5 years, the lowest since 2019.(1) Activism, meanwhile, stayed at the high end of its decade-long range, with 141 US campaigns in 2025, the most in any year of the past decade.(2) That pace has continued into 2026. Through June, US campaign activity was running about 9% ahead of the same point in 2025. The rise has been steepest among the largest companies, where campaigns at US targets above $5 billion grew about 63% from 2021 to 2025, nearly double the pace of the broader market, and are running 19% ahead of last year so far in 2026.

These trends have also weighed on CEOs. An activist approach today is associated with a meaningfully higher chance of an early CEO departure than it was five years ago, closer to one in five than the one in twenty of a few years back.(3) And this trend has not spared new CEOs. Where activists once gave a new leader room to settle in, many now see a leadership change as a natural moment to engage, and the data reflects it. This note looks at three things worth understanding early: how soon real scrutiny tends to arrive, why a leadership transition can attract attention rather than shield against it, and why understanding your own shareholder base early matters as much as anything.

Tenure and Timing

It helps to start with the tenure picture, which rewards a little care, because two measures point in different directions. The standing population of sitting CEOs has held up well. Across the S&P 1500, the average sitting CEO has about eight years in the role (median of six), and that figure has drifted up over the past decade rather than down, helped by a long tail of veteran founders and owner-operators.(2) The shift appears at the exit. The average tenure of departing S&P 1500 CEOs has come down from a peak of 10.3 years in 2021 to 8.5 in 2025.(1) For someone stepping into the role, the encouraging standing average is less relevant than the simpler reality that departures are coming a little sooner than they used to.

There is a sensible logic to when the pressure tends to build. Spencer Stuart's CEO life cycle research describes how the early optimism gives way to closer assessment. Roughly 88% of new CEOs come through the first year, but about a quarter have moved on by the end of year three and half by the end of year six, with the highest single-year rate of departures in year four.(4) Much of this traces to year three, when a CEO's early moves have had time to show results and the market begins to form a firmer view.

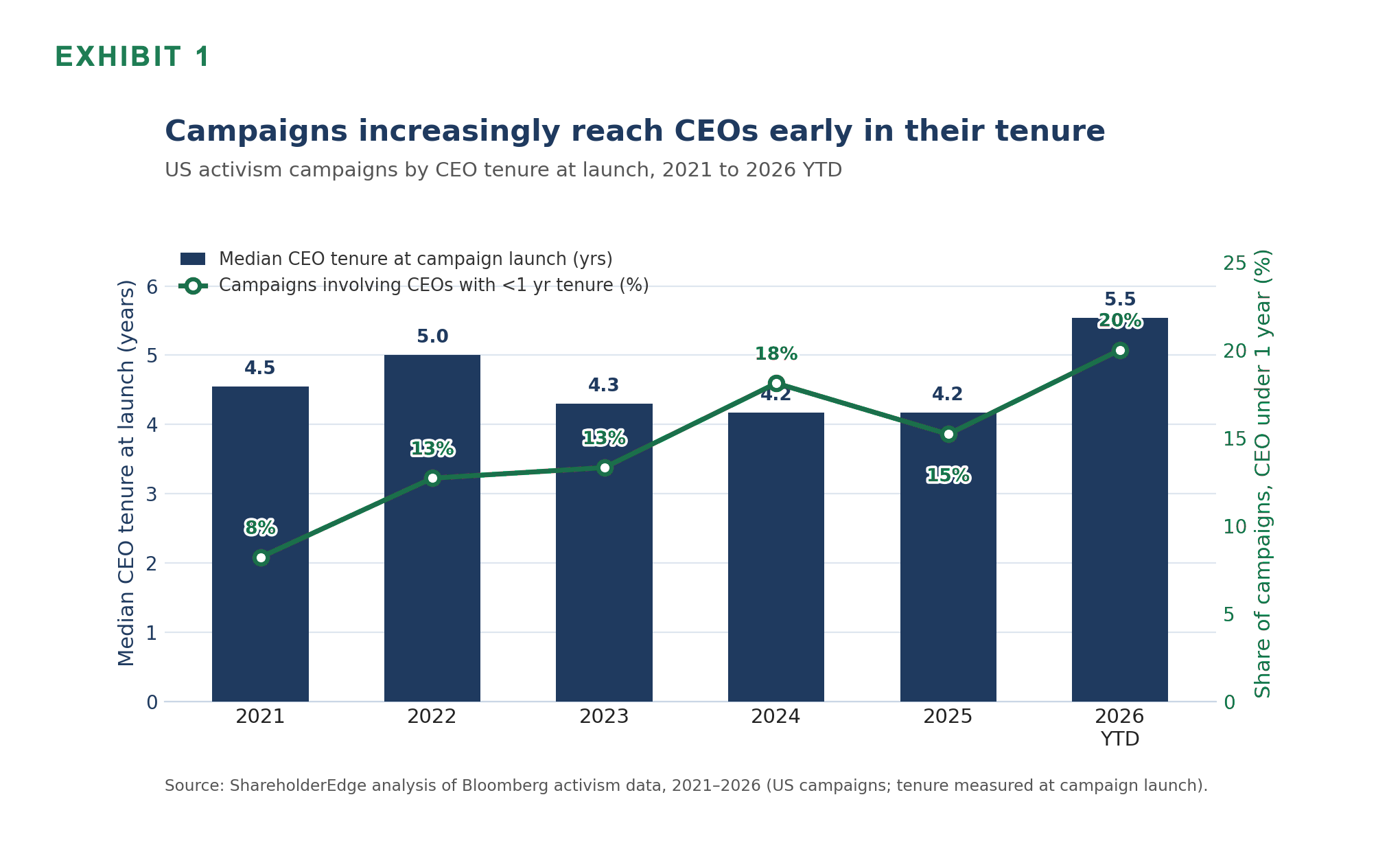

Activists tend to engage right around this same window. Over the past five years, campaigns have surfaced publicly at companies with a median CEO tenure of roughly 4.4 years, ranging from 4.2 to 5.0 in any given year.(2) That falls in the stretch where assessment is sharpest, after the early optimism has settled and before a CEO has built up the credibility of a long track record. It also reflects tenure only at the moment a campaign becomes public. Allowing for the time an activist usually spends building a position and engaging privately beforehand, the point at which a company first draws attention is likely closer to three to four years.

The pressure reaches earlier still. Over 2021 to 2025, campaigns involving a CEO with less than a year in the role averaged about 13.5% of the total, and that share has risen from 8% in 2021 to 20% so far in 2026. In practice, a new CEO is being assessed from early on.

The transition itself often opens the door. A leadership change gives an activist a natural argument to make: that the board may not have chosen the right person, and that a fresh outside perspective could help. That argument tends to find a receptive audience among unaffiliated investors. The pattern is visible in our own campaign data, where the share of campaigns reaching CEOs in their first year has moved up over the past five years, as Exhibit 1 shows.

The Inherited Shareholder Baase

A new CEO inherits a strategy, a board, and a management team. They also inherit a shareholder base.

New CEOs Should Know More About Their Investors

Given all of this, a lot of new CEOs want a clear-eyed read on their vulnerability to activism early, often in their first few months in the role. That instinct is a sound one. In my experience the exercise earns its keep when it goes past performance and capital allocation and looks honestly at how the company’s own shareholders see it.

A new CEO inherits a strategy, a board, and a management team. They also inherit a shareholder base, and it deserves the same attention as everything else. The sooner you understand who owns the stock and why, the better placed you are to anticipate how the market is likely to receive your early decisions.

The steps below are how I approach that in practice, and they are the same questions I work through with the companies I advise. They are worth running on your own, whether or not you ever bring in outside help.

Start with a simple split: which of your investors have a choice, and which do not. For example, one group holds your stock because they want to. Hedge funds and growth investors are there on conviction, with high expectations for performance and limited patience when it slips. Another group may hold your stock because they more or less have to. Index funds own it because it sits in their benchmark. Active mutual funds that are underweight hold a token position they would rather avoid. Dividend-focused investors are there for the payout and often expect little beyond its continuation.

That second group is now very large, driven by the growth of index funds, and generally holds a significant portion of companies that have underperformed their peers on TSR. Passive funds overtook active funds in US equity assets in 2024 and have kept gaining share.(5) BlackRock, Vanguard, and State Street together hold roughly a fifth to a quarter of the shares of most companies in the S&P 500 and the broader S&P 1500, and they are the single largest shareholder in more than nine of ten companies in both.(2) In the S&P 500, where their stakes run highest, they also cast about a quarter of the votes at company meetings.(6)

One point is worth dwelling on. The captive holders are usually not the ones raising concerns in your investor meetings. They rarely push back on performance, since selling is not really an option for them, and it is easy to read that quiet as contentment. It often is not. When an activist does run a campaign, those same holders frequently decide the outcome. They are not predisposed to support a dissident. Vanguard, for instance, supported an activist nominee in only about one in five contested cases from 2022 to 2024.(7) But they hold the deciding votes, and they will get behind what they perceive as a credible case for change, as Engine No. 1 showed at ExxonMobil with a small stake and the index funds alongside it.

Next, it helps to understand why some investors avoid your stock. The reasons tend to fall into two camps. The first is the good company that is not a good stock, where the business is sound but the valuation already prices in the good news, so the forward return sits below what investors require. The second is the company people have lost some faith in, where the stock looks cheap on paper but the story does not yet earn enough trust to own. These call for very different responses, so it is worth knowing which one you are facing.

Then map what investors actually expect from your strategy. What do they believe your priorities should be if you are going to deliver above-average returns? Once you have a feel for that, you can anticipate how they will react to your next move rather than be surprised by it. Will the stock rise if you announce a cost-cutting program? Will it fall if you announce a large acquisition? The answers are company-specific, and they have often surprised CEOs I have advised.

It is also worth understanding the alignment between investors and the prior management team. Did the last CEO deliver the returns investors expected? Did investors believe in that strategy and in management's ability to execute it profitably? The answers shape how investors will see you. They will either welcome someone to drive change they can get behind, even if it unsettles the status quo, or they will prefer continuity and a steady hand on the existing plan. This matters a good deal if you are weighing any kind of strategic shift, because it tells you how best to frame that shift for the market.

Finally, it helps to remember that investors are wary of heavy-investment phases, which usually compress near-term returns. If your company is heading into one, the first communication priority is not the vision itself. It is showing investors, concretely, how that spending will earn a return above its cost of capital. Make that case well and you earn the room to invest. Leave it unmade and you create the kind of gap an activist tends to notice.

Staying Close to Shareholders

The same pattern runs through the data. CEOs are turning over somewhat faster, activists are engaging earlier in a tenure, and the effects on the chief executive are meaningful. Over the past two years, about one in five companies that drew an activist saw its CEO depart within a year of the campaign becoming public, compared with roughly 12% of S&P 500 CEOs in a typical year. In 2025, 32 US CEOs resigned within a year of a campaign, the most on record.(8) With activism at high levels and likely to continue into 2026, this is not a dynamic that seems set to ease soon.

For a new CEO, a few practical implications follow. The three to four years it takes to prove a thesis is a genuine window, though not a period of guaranteed patience, and assessment really does begin early. The shareholder base, much of it quiet and easy to overlook, tends to decide any contest, so it is worth understanding and engaging well before one arises rather than in the middle of it. And since the market rewards capital discipline and is wary of undisciplined spending, a clear and credible account of returns on capital is among the most durable forms of preparation a CEO can have. The first year is less a honeymoon than it once was, and it may be the most consequential stretch of the job.

None of this is only for the first year, or only for first-time CEOs. Whether you are arriving from another corner office or taking the role for the first time, and whether you are in your first quarter or your tenth year, the same questions are worth asking. And if it is work you have not yet done, it is never too late to begin. Shareholder bases turn over, expectations shift, and the investors who supported you in the past may see things differently now. Staying close to who owns your stock and what they expect is less a one-time exercise at the start of a tenure than a habit worth keeping. In my experience, the CEOs who treat it that way are rarely the ones caught off guard.

Footnotes

(1) Spencer Stuart, 2025 S&P 1500 CEO Transitions: Behind the CEO Moment, January 2026.

(2) ShareholderEdge analysis of Bloomberg data. Campaign counts cover US companies above the stated market-capitalization threshold at announcement (above $500 million unless noted), exclude closed-end funds, and count one campaign per company. Tenure figures cover S&P 1500 CEOs, both sitting and at the point of a campaign, 2016 to 2026. Combined BlackRock, Vanguard, and State Street ownership across the S&P 500 and S&P 1500, and their standing as the single largest holder in each.

(3) Fortune, on the collapse of CEO tenure, December 2025.

(4) Claudius A. Hildebrand and Robert J. Stark, The Life Cycle of a CEO (Spencer Stuart).

(5) Morningstar, on US passive fund assets surpassing active in 2024.

(6) Edwin Hu, Robert E. Bishop, and Frank Partnoy, "Mirror Voting," ECGI Law Working Paper No. 940/2026 (2026).

(7) Vanguard voting disclosure, cited in Columbia Law School research on activist proxy contests, 2022 to 2024.

(8) Cleary Gottlieb, 2025 Shareholder Activism Trends and What to Expect in 2026, January